The 114th episode of my weekly YouTube show where I discuss what is happening in investment markets and what to look out for. This week I explain how and why the market is trying to tell us something.

Each show lasts between 5-10 minutes and is aimed at DIY investors (including novices) seeking contemporary analysis to help them understand how investment markets work.

Subscribe to my YouTube channel to receive my weekly analysis of investment markets or alternatively, you can listen via my weekly Midweek Markets podcast below.

Midweek Markets weekly podcast

Other ways to watch, listen and subscribe

You can listen to other episodes and subscribe to the show by searching 'Money to the Masses' on Spotify or by using the following links:

Abridged transcript - Midweek Markets episode 114

Hello, and welcome to the latest episode of Damien's midweek markets, the show where I tell you what's been going on in investment markets, and what to look out for in the days and weeks ahead.

If we look at the market it seems to be trying to send a message. The NASDAQ 100 is up about 2.3% so far in July. Over the same period the German DAX is up 1.2% while European stocks are broadly up 1%. If you look at the MSCI AC World Index it’s up 0.6%. The Dow Jones is broadly flat, while the FTSE 100 is down 0.48%. And then you've got emerging markets down around 2% along with Asian equities. So you can see a real divergence has occurred over the last couple of weeks. And if you delve deeper, then you'll notice some other interesting things are going on in markets.

For example, if you look at bank stocks ($xlf) in the S&P 500 and compare them to the tech stocks ($xlk) within the same index then you see that big tech stocks are now outperforming. If you recall, the reflation trade so far this year had been about financials and cyclical sectors outperforming sectors that normally perform poorly in a rising interest rate environment. The latter group includes tech stocks and growth stocks. But what we've seen since the US Federal Reserve meeting in June is large tech stocks now outperforming financials. That is despite some strong earnings reports from the banking sector this week. Is the reflation trade dead?

So for those investing in funds or ETFs, that favour value/cyclical sectors, including bank stocks, they are left wondering what's going to be the catalyst to push them higher. But while growth stocks have outperformed value stocks over the last month, even they have begun to stall. Is the market finally running out of steam?

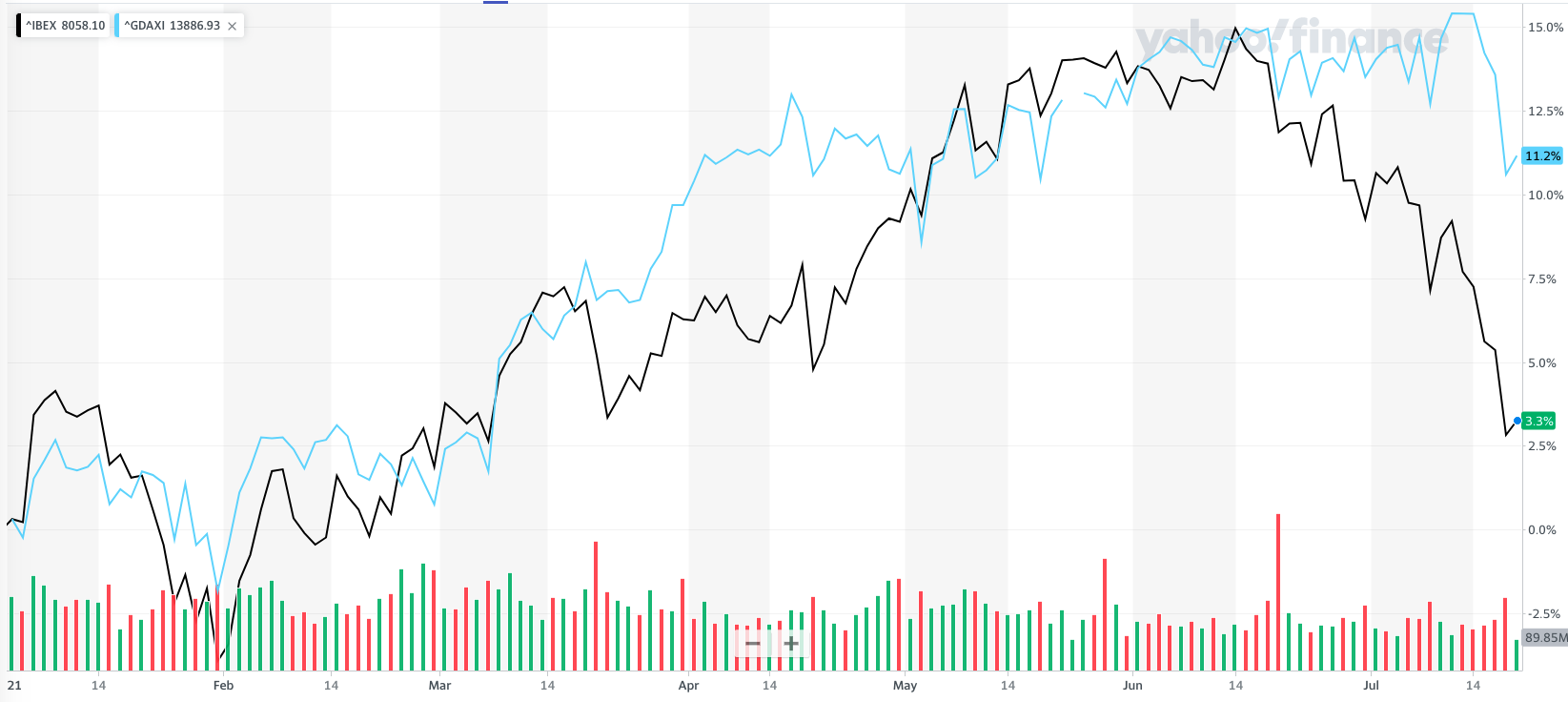

Cracks are also starting to show in European stocks too. Until mid-June (the Fed meeting) the German DAX and the Spanish IBEX had been moving in lockstep. But in the last few weeks this relationship has broken. The IBEX has begun to crash lower, while the DAX has continued to hold up (see below):

One possible explanation for the divergence could be that the ability for global economies to fully reopen, and therefore fully recover from the pandemic-slump, is being called into question as COVID cases continue to rise thanks to the delta variant. With Spain being a popular holiday destination, particularly for UK tourists, travel restrictions imposed by respective governments will inevitably hit tourism and therefore the Spanish economy.

But how long can the IBEX continue to tumble without it having a wider impact on the rest of Europe, including the German DAX?

If we now look at other sectors we can see that real estate (REITs) have started to perform well. You can track the price moves in real estate equities in the US by looking at $xlre. Real estate stocks derive some of their value from the yield they can offer. In a world where interest rates are rising, then they aren't particularly attractive. So what we're seeing is that REITs are outperforming in a world where we're seeing yields starting to fall. It suggests that the market thinks that central banks won’t be able to raise interest rates due to the fragility of economic growth.

If we look at the 10 year US Treasury yield over the last couple of weeks, we hit a short-term high of around 1.45%. But then we saw a rapid repricing of bonds. Investors started buying bonds, and it caused the 10 year US Treasury yield to crash down to 1.25%, which was a four-month low. That was a big move. And then we saw a bit of a rebound from its 200 day moving average. But the sudden. demand for bonds has made equity markets sit up and pay attention.

The fall in bond yields has also been good for gold, allowing it to bounce back above $1,800 per ounce. If it can maintain momentum and close above $1,850 it would bode well for the precious metal from a technical perspective.

So if you pull everything together, the fact that tech stocks are outperforming financials, divergences in European equities, that we're seeing treasury yields tumble, that we're seeing gold having another lease of life... all of this starts to suggest that markets are telling us something. Is it that the market believes that inflation is indeed transitory, despite new official data in the UK and the US showing inflation is still increasing?

It could also be a sign that the market is pricing in the likelihood that we are moving into a new economic phase of slowing economic growth, following the post-pandemic rebound? If any of these assumptions are challenged then we could see a rapid repricing of markets again. But for now, the reflation trade looks to be in terminal decline.

Before we finish, from a technical analysis perspective the S&P 500 is pushing up towards the 4400 level. Keep an eye on that because the 4400 level is going to be key. If you're into Fibonacci extensions, and you use the COVID sell-off as your starting point it suggests that the upside high point, at least in the short term, is going to be 4400. At that point the index is likely going to struggle to break through that level. If it does that would set up for a much bigger move higher. But in the short-term the market looks tired.

The big things to watch out for in the coming days and weeks are the stories around COVID infection levels, company earnings reports, central bank soundbites but also pay particular attention to the 10 year US Treasury yield, because that seems to be driving a lot of what's going on in markets right now.

MTTM AI (beta)

MTTM AI (beta)