On Monday, swaps markets were pricing in four Bank of England (BoE) rate rises in 2026, a significant jump from the two rate increases predicted following last week's BoE's rate-setting meeting, when it held the base rate at 3.75%.

On Monday, swaps markets were pricing in four Bank of England (BoE) rate rises in 2026, a significant jump from the two rate increases predicted following last week's BoE's rate-setting meeting, when it held the base rate at 3.75%.

The good news is that investors have rowed back on their predictions, but the bad news is that markets are still predicting two to three 0.25% increases this year, taking the base rate from 3.75% to at least 4.25%.

Why are investors predicting rates will go up?

Last week, the Monetary Policy Committee (MPC) at the Bank of England (BoE) voted to hold the base rate at its current level of 3.75%, a decision that few would have predicted prior to the initial US-Israeli attack on Iran, when a 0.25% cut seemed a certainty. Now, with the UK seemingly on the brink of a sharp rise in inflation, the market expects the BoE to have to raise interest rates this year.

Although the Bank of England cannot control global economic crises, it will be expected to react to the threat of spiralling inflation. Higher global gas and oil prices, triggered by the war, will push up energy costs and the price of everyday goods and services, with some predicting a 4% inflation rate in the second quarter of 2026.

By voting unanimously, the MPC also signalled to investors that the Bank's approach to the Middle East crisis would be cautious, with it waiting for events to unfold before it signals its next move. This led many to the conclusion that escalations in the conflict will mean a rate increase, or even several. With Trump threatening over the weekend to "obliterate" Iran’s energy infrastructure if it did not allow shipping to move through the Strait of Hormuz before a deadline on Monday, investors began betting on rising prices requiring four 0.25% base rate increases before the end of 2026.

Sentiment shifted, though, when the US president postponed the threatened attack on Iranian energy infrastructure for five days, claiming "productive" talks had taken place. The market immediately reduced the number of predicted BoE rate hikes in line with the perceived reduction in the size and duration of any potential inflation shock. However, Iran has since denied that any talks have taken place and fixed mortgage rates continue to rise in the UK, with all sub-4% fixed mortgage deals disappearing in recent days.

But some economists predict rates will not go up

In contrast to the sharp movements in the market's interest rate predictions, some economists are still not expecting any base rate increases this year. While the Middle East conflict is dominating the news cycle, there is an argument that serious domestic issues that could balance out war-propelled price pressures may have slipped under the radar.

Weak economic growth and employment levels had been expected to pull inflation down below the Bank's 2% target in the medium term well before war broke out, and events abroad have done nothing to improve either area. This could mean that while the conflict drives inflation up, weak spending power pulls it back down.

Andrew Wishart, economist at Berenberg, said that persistent inflation is "only plausible when firms have pricing power and workers have bargaining power" but that "neither is the case now". In a note to clients published on Friday, Goldman Sachs said: "Our economists now think that the MPC will remain on hold for longer and maintain at 3.75% throughout 2026."

There have also been suggestions that the market has over-represented the hawkishness of the Bank's decision to hold rates last week. While it did position itself as "ready to act as necessary", the MPC consensus came from a desire to 'wait and see' and "assess how events unfold", according to the Bank of England governor Andrew Bailey.

Where will interest rates go in 2026?

The path for interest rates in 2026 will likely be shaped by events in the Middle East, though the domestic economy will have a part to play. The reopening of trade routes and a major de-escalation in the Middle East could ease price pressure at home and dramatically change the global economic outlook. However, an escalation of attacks on energy production sites would likely see a return to the sort of position seen on Monday morning, when multiple rate hikes were priced in. The performance of the UK economy will also come into the equation, with the potential for unemployment and weak growth to pull inflation down.

As we have seen in recent weeks and days, predictions have not lasted very long and have been easily shaped not just by global events, but by commentary, claims and counter-claims from both sides.

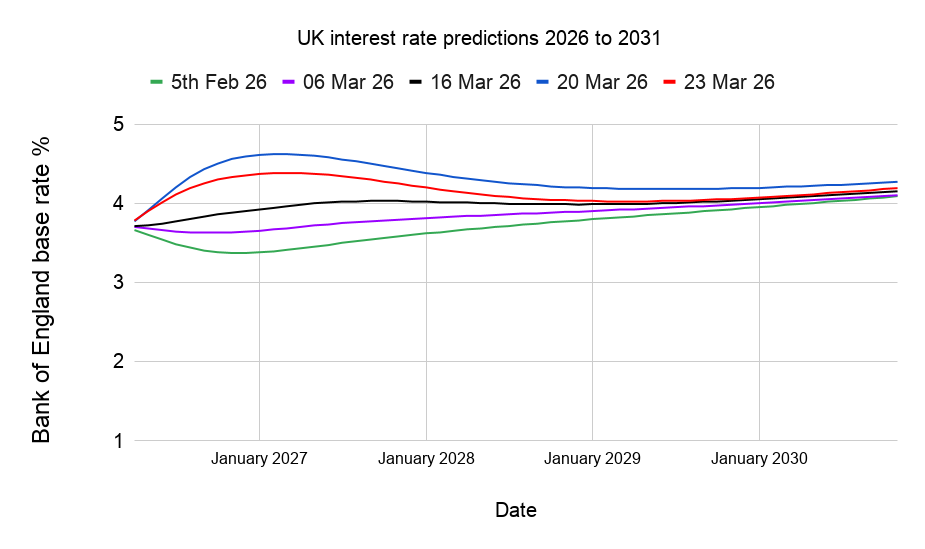

You can see from the graph below, based on data available on Monday, not just how sharply rates are expected to rise, but also how dramatically predictions have shifted in just a few weeks. Each coloured line represents the market's prediction, made on the stated date, of where the BoE base rate will be over the next five years.

If you are interested in learning more about where interest rates might go in the future, check out our article on the latest UK interest rate predictions.

What is happening to mortgage rates?

Mortgage lenders are responding to the volatile global situation by pulling hundreds of products from the market and repricing. The average two-year fixed mortgage rate hit 5.43% on Monday, its highest point since February 2025, and 0.6 points higher than at the start of March.

There are approximately 1.8m households due to remortgage this year. Many of them will be coming off five-year fixed-rate deals secured when rates were significantly lower than what anyone would be able to get today.

With so much uncertainty, mortgage holders whose current deals are due to expire this year should start shopping around for a new mortgage rate. Remortgage deals can usually be secured up to six months in advance, depending on your lender. If you plan to search the market for the best remortgage deal, you may find it helpful to speak with a mortgage broker who can help you to secure a deal. You can find one by searching the online professional directory, Vouchedfor*, where you will find professional mortgage brokers in your area. The directory breaks mortgage brokers down by specialism and you can view other customers' reviews of the service that they have provided. Alternatively, you can access mortgage advice online and over the phone through the online mortgage broker Habito*. Habito's mortgage brokers can search over 90 lenders' mortgage deals and will provide advice and guidance to help you secure your mortgage offer.

You can also check the new deal offered by your lender against the best deals on the market, which we regularly update in our article, 'Best remortgage deals in the UK'.

Help if you're unable to afford your mortgage payments

Many mortgage holders continue to face rising mortgage costs due to the rise in mortgage interest rates since 2021. If you are worried about how you will afford your mortgage, then you should get in touch with your lender as soon as possible. Your lender should be able to find a solution that can help ensure no repayments are missed.

Potential solutions can include extending the length of your mortgage, converting part or all of your repayment mortgage to an interest-only mortgage or allowing you to take a mortgage payment holiday.

Check out our article 7 tips for dealing with mortgage arrears, or alternatively, you may find additional support from the following organisations helpful:

If a link has an * beside it this means that it is an affiliated link. If you go via the link, Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. The following link can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers - Habito, Vouchedfor

MTTM AI (beta)

MTTM AI (beta)