On Sunday, the United States and Iran announced a preliminary peace deal aimed at ending the Middle East conflict. The memorandum of understanding promises to halt hostilities, lift naval blockades and reopen the Strait of Hormuz, a vital trade route that handles roughly 20% of the world's daily oil and seaborne liquefied natural gas (LNG) exports. Since the conflict escalated in March 2026, global energy and shipping markets have been in turmoil, pushing up the cost of living and threatening a renewed inflation crisis.

On Sunday, the United States and Iran announced a preliminary peace deal aimed at ending the Middle East conflict. The memorandum of understanding promises to halt hostilities, lift naval blockades and reopen the Strait of Hormuz, a vital trade route that handles roughly 20% of the world's daily oil and seaborne liquefied natural gas (LNG) exports. Since the conflict escalated in March 2026, global energy and shipping markets have been in turmoil, pushing up the cost of living and threatening a renewed inflation crisis.

The recent diplomatic breakthrough has brought a huge wave of relief to global financial markets. Here is a breakdown of what the peace deal means for your household finances, from your energy bills to your pension.

Energy bills

The effective closure of the Strait of Hormuz in March 2026 caused a major energy shock, driving oil prices from approximately $70 a barrel of Brent Crude to over $120 a barrel at its peak. Since the peace deal announcement, the price of oil has fallen back to $80 a barrel. If this fall is sustained, then it should see the wholesale cost of energy start to fall, leading to a drop in household energy bills for UK consumers.

Although the energy price cap is already scheduled to rise by £221 on 1st July, any easing of wholesale energy costs would mean that future price cap predictions for October 2026 and beyond will be revised downwards.

Prior to the news of the peace deal, the energy price cap was predicted to rise 2-3% in October 2026, as shown in the chart below. If energy prices do begin to fall then we could expect to see the energy price cap move back towards £1,641 (its current level which was set prior to the start of the war). However, even if the Strait of Hormuz is fully reopened, oil production in the Middle East is not expected to return to its pre-war level for months, which will likely mean that the price of oil and LNG will remain elevated for some time.

Petrol & Diesel prices

The rise in petrol and diesel prices, as a result of the war in the Middle East, had the most immediate impact on UK consumers' finances, which also contributed to a rise in UK inflation. The chart below shows how the price of diesel rose by almost 50p per litre at its peak, before easing. While the rise in the price of unleaded petrol was lower, it remains much closer to its peak.

If the Strait of Hormuz reopens and the production of oil eventually returns to levels seen earlier in 2026, then the price of fuel at the pumps should start to fall, potentially cutting the cost of filling up a family car by £11 to £16 per tank.

Mortgage rates

The Middle East conflict caused severe turmoil in the mortgage market, which led to fears that the average monthly mortgage payment could jump by £300. In the worst-case scenario, UK inflation was predicted to rise as high as 6.2%, well above the Bank of England's (BoE) 2% target. The prospect of the BoE raising interest rates to combat rising inflation had an immediate impact on the mortgage market, with lenders pulling deals and increasing rates.

To better communicate the possible future path of inflation and the base rate, at its last rate-setting meeting in April, the BoE set out three possible scenarios for the UK economy, which were dependent on the price of oil.

The table below shows the estimated increase in mortgage payments for a typical borrower with a £250,000 mortgage over 25 years. Under this example, the pre-Iran war average mortgage rate was 4.89%, meaning that the monthly mortgage payment was £1,445.

| Scenario | Oil price assumption | Inflation outlook | BoE base rate impact (currently 3.75%) | Estimated new average mortgage rate (currently 4.89%) | Annual cost increase (vs pre-conflict) | Monthly payment increase (vs pre-conflict) |

| Best Case (Scenario A) | Oil price falls back below $80 a barrel by end of 2026 | Peaks at 3.6%, falls below 3% | Stability with cuts sooner | 5.0% - 5.5% | +£150 to £1,050 a year | up to £88 a month |

| Most Likely (Scenario B) | Oil price stays above $80 a barrel | Peaks at 3.7%, stays elevated | Higher for longer | 5.5% - 6.0% | +£1,050 to £1,950 a year | up to £163 a month |

| Worst Case (Scenario C) | Sustained oil price above $120 for rest of the year | Peaks at 6.2% | Rises to 5.25% | 6.75% | +£3,380 a year | up to £282 a month |

At the time, Andrew Bailey said: "...I place most weight on Scenario B, albeit with slightly reduced second-round effects. I place some weight on Scenario C, which would require a stronger monetary policy response."

However, if the peace deal holds and the price of oil remains below $80 a barrel then the Best Case (Scenario A) now becomes the most likely outcome. That means the BoE would be unlikely to raise the base rate, which in turn would mean that average mortgage rates would stabilise around 5%, and the best-buy deals would start to fall.

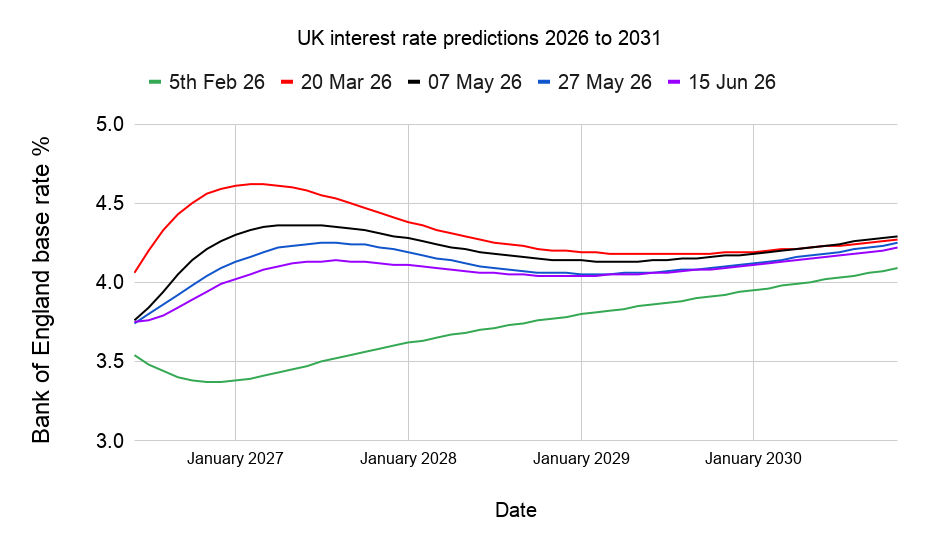

In the last 48 hours, the market has revised its prediction for the path of the BoE base rate over the next five years. Each coloured line on the chart below shows the prediction made on the stated date of where the base rate would be over the following five years. The red line shows the market prediction at the height of the war, when it was anticipated that the BoE would raise the base rate four times, to 4.75%. The purple line is the latest prediction, and the market now anticipates just one rate rise in 2026.

At present, mortgage lenders have yet to react to the fall in interest rate expectations. However, if base rate expectations continue to fall then fixed mortgage rates should too. Currently, the best two-year fixed rate mortgage is approximately 0.5% higher than the equivalent rate prior to the start of the war.

Savings account interest rates

While mortgage rates have yet to react to the news of a peace deal, interest rates on savings accounts have already begun to fall. When the market was bracing for base rate hikes, savings rates became more competitive.

Now that the prospect of multiple rate increases is fading, banks and building societies are likely to begin withdrawing their top-paying accounts, with the interest rates on the top-paying easy access cash ISAs already falling by as much as 0.4% in the last few days. If you have cash to put away, now may be a good time to act before the best deals disappear. Bookmark our best-buy cash ISA table and our fixed-rate Cash ISA best-buy table.

Investments & pensions

The apparent resolution of the conflict sparked a significant stock market bounce, particularly in regions most reliant on Middle East oil exports. This is evident in the table below, which shows the stock market moves of major global stock markets in the 48 hours after the peace deal was announced.

Asian and emerging market equities enjoyed the strongest rallies, while the FTSE 100 lagged as energy company share prices fell alongside the price of oil, an area of the market the FTSE 100 has exposure to.

| Index | % increase in the two days after the peace deal announced |

| Nikkei 225 (Japan) | 5.13 |

| MSCI AC Asia ex Japan | 3.39 |

| MSCI Emerging Markets | 3.18 |

| Nasdaq 100 (US-tech) | 3.06 |

| S&P 500 (main US index) | 1.08 |

| FTSE Eurofirst 300 (European index) | 0.48 |

| FTSE 100 | 0.21 |

Meanwhile, government bond yields fell, meaning that bond prices rose. Rising stock markets and bond markets are good news for consumers investing via a Stocks and Shares ISA or a pension.

MTTM AI (beta)

MTTM AI (beta)