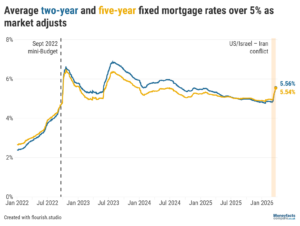

The average two-year fixed-rate mortgage is now more expensive than the average five-year fixed-rate deal, according to data from Moneyfacts. The two-year average is now 5.56%, just above the typical rate charged for a five-year fixed deal of 5.54%.

The average two-year fixed-rate mortgage is now more expensive than the average five-year fixed-rate deal, according to data from Moneyfacts. The two-year average is now 5.56%, just above the typical rate charged for a five-year fixed deal of 5.54%.

This represents both an inversion of the pattern of recent months and a sharp increase in the cost of both types of product. Five-year deals had been more expensive than two-year options because of the expected short-term outlook for interest rates. Just a few weeks ago, at the start of March, the two-year average deal charged 4.83% interest, while the five-year average was 4.95%.

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, said: "In a traditional market, the average two-year fixed deal would be lower than the five-year, but the unrest in the Middle East is causing concerns over the path of interest rate setting, with inflation expected to spike in the months ahead."

Why is the average two-year fixed-rate mortgage now more expensive than a five-year fix?

The mortgage market is reacting to the current intense uncertainty over interest rates and inflation. Cheaper deals are available on longer fixed terms in anticipation that rates will move back downwards after the current period of extreme short-term volatility ends.

Short-term predictions are very difficult to make at the moment, with energy market turmoil caused by the war in the Middle East triggering a global economic shock that could provoke another cost-of-living crisis in the UK. Oil prices have soared above $100 a barrel and European gas prices have almost doubled, amid warnings that a prolonged conflict could have far-reaching effects on global living standards. On 23rd March, the Monetary Policy Committee (MPC) at the Bank of England (BoE) voted to hold the base rate at its current level of 3.75%, a decision that few would have predicted prior to the initial US-Israeli attack on Iran, when a 0.25% cut seemed a certainty.

Now, with the UK seemingly on the brink of a sharp rise in inflation, the market expects the BoE will raise interest rates at least twice this year. However, this spike is expected to be followed by a downward trend and period of stability. You can learn more about where interest rates might go in the future on our latest UK interest rate predictions page.

Mortgage rates followed a similar pattern in late 2022, when the now infamous 'mini-Budget' triggered a financial crisis. The inverted market held for almost three years, until August 2025, as you can see in the Moneyfacts graph below:

Disappearing mortgage deals

Another factor in the inversion of the mortgage market is the 1,500 mortgage products withdrawn from the market in the last three weeks. According to data collected by Moneyfacts, a fifth of the overall market has disappeared since 9 March 2026, including 448 deals on 21st March alone - a single day figure only beaten by the 2022 mini-Budget fallout.

This leaves borrowers with both fewer deals to choose from and facing higher rates from what is left on the market.

How long should you fix your mortgage for?

How long you should fix your mortgage for will depend on your own financial situation and priorities. If your current deal is due to expire this year, and with so much uncertainty, it is a good idea to start shopping around for a new mortgage rate and assessing your options.

Remortgage deals can usually be secured up to six months in advance, depending on your lender. If you plan to search the market for the best remortgage option, you may find it helpful to speak with a mortgage broker who can help you to secure a deal. You can find one by searching the online professional directory, Vouchedfor*, where you will find professional mortgage brokers in your area. The directory breaks mortgage brokers down by specialism and you can view other customers' reviews of the service that they have provided.

Alternatively, you can access mortgage advice online and over the phone through the online mortgage broker Habito*. Habito's mortgage brokers can search over 90 lenders' mortgage deals and will provide advice and guidance to help you secure your mortgage offer.

You can also check the new deal offered by your lender against the best deals on the market, which we regularly update in our article, 'Best remortgage deals in the UK'.

If a link has an * beside it this means that it is an affiliated link. If you go via the link, Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. The following link can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers - Habito, Vouchedfor

MTTM AI (beta)

MTTM AI (beta)