The Bank of England (BoE) has taken the decision to raise the base rate of interest by 0.25%, taking it from 4.00% to 4.25%. It is the 11th consecutive base rate rise since rates started rising in December 2021. In this article, we explain the likely impact that the latest base rate rise will have on both savers and borrowers. We've also included some additional resources and tools to help those that are hoping to remortgage soon.

What is the Bank of England base rate?

The Bank of England base rate is the rate that the Bank of England charges banks, building societies and other lenders when they borrow money. A rise to the Bank of England base rate causes a knock-on effect, meaning banks and other lenders need to raise the interest rate that they charge borrowers, to ensure they continue to make a profit and cover costs. Conversely, savers are likely to see savings rates increase across the market, although this isn't guaranteed for every lender and the rate offered will often be far lower than the rate charged to borrowers, again, ensuring the lender makes a profit.

Why has the Bank of England base rate increased?

The Monetary Policy Committee (MPC) voted to raise the Bank of England base rate by 0.25% following news that inflation unexpectedly rose to 10.4% in February, up from 10.1% in January. With the base rate now at 4.25%, consumer borrowing and spending should start to slow, encouraging even more people to save. It is hoped that the latest interest rate rise will help to cool inflation as we move towards Summer 2023.

Looking at the wider picture, things are harder to predict. A lot will depend on the health and stability of the banking sector following the failure of Silicon Valley Bank (SVB) and the government rescue of Swiss bank Credit Suisse.

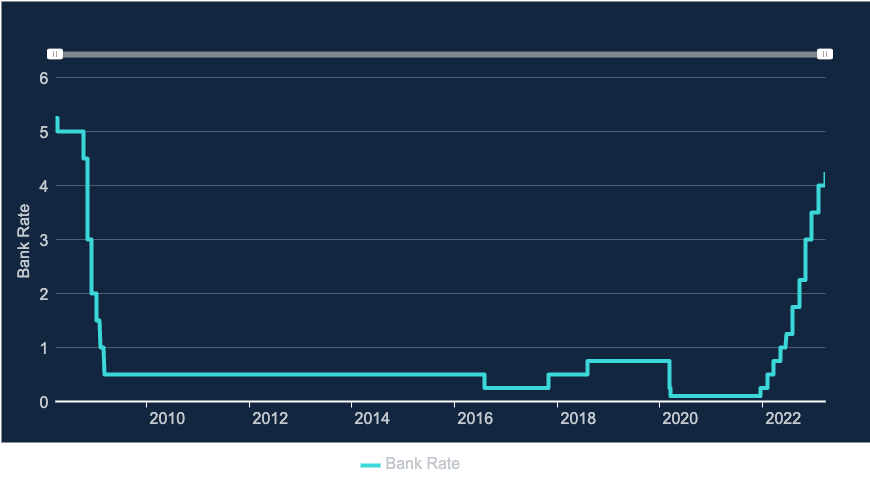

The following graph shows how the Bank of England base rate has increased over time.

(Source: Bank of England)

Rate rises and how they impact you: December 2021 - March 2023

The latest Bank of England base rate increase is expected to help slow down inflation amid increasing fears over the global banking system after two large US banks recently failed. Below, we provide a summary of the Bank of England base rate rises since December 2021.

| Date | Interest rate rise | Previous interest rate | New interest rate | Increase to average monthly mortgage repayments per £100k borrowed* |

| 16th December 2021 | +0.15% | 0.10% | 0.25% | £8 |

| 2nd February 2022 | +0.25% | 0.25% | 0.50% | £13 |

| 17th March 2022 | +0.25% | 0.50% | 0.75% | £13 |

| 5th May 2022 | +0.25% | 0.75% | 1.00% | £13 |

| 16th June 2022 | +0.25% | 1.00% | 1.25% | £13 |

| 4th August 2022 | +0.50% | 1.25% | 1.75% | £26 |

| 22nd September 2022 | +0.50% | 1.75% | 2.25% | £26 |

| 2nd November 2022 | +0.75% | 2.25% | 3.00% | £39 |

| 15th December 2022 | +0.50% | 3.00% | 3.50% | £26 |

| 2nd February 2023 | +0.50% | 3.50% | 4.00% | £26 |

| 23rd March 2023 | +0.25% | 4.00% | 4.25% | £13 |

| TOTAL | £216 |

*assumed mortgage term is 25 years

How does the BoE interest rate rise affect you if you have a mortgage?

Fixed-rate mortgage customers

Roughly 75% of mortgage holders are on a fixed-rate mortgage deal, protecting them, for the time being at least, from the latest interest rate rise. If your fixed-rate deal is coming to an end in the next 6 months then you may wish to read our article 'Remortgaging in 2023 – is now the right time to fix & for how long?'. Those on a fixed deal that is coming to an end should consider the impact that the latest rise has on them and budget accordingly. As a rough guide, the 0.25% rise will mean the monthly mortgage repayments will rise by around £13 per month for every £100,000 you owe, based on a 25-year mortgage length. However, the figures are only based on the latest base rate rise, so if your current fixed-rate deal was in place before December 2021, you will need to include the cost of all of the rate rises combined. This works out at an increase of roughly £216 per month, per £100,000 borrowed, based on a 25-year mortgage term.

Variable rate or tracker mortgage customers

Those with tracker or variable rate mortgages are likely to see their mortgage payments increase in line with the latest Bank of England base rate announcement, however, lenders often take time to implement the increase, so exactly when you will feel the increase will depend on your lender. You can work out what the impact will be on your mortgage payments by using our interest rate rise calculator. You'll need your mortgage term, mortgage balance and the current interest rate figures.

Anyone worried about the impact that the latest base rate rise will have on their finances should speak with an independent mortgage adviser* as they can easily explain the likely impact on your finances as well as the best way to remortgage. They will be able to weigh up your options and compare what mortgage rates and deals are available to you. Always check to see if there are any Early Repayment Charges (ERC) when remortgaging and check to see how long is left on your current deal. Alternatively, you can take a look for yourself by using our mortgage best buy calculator.

How does the BoE interest rate rise affect you if you have credit cards, loans or overdrafts?

Credit cards

If you have an existing credit card with an agreed interest-free period or promotional interest rate, the latest Bank of England base rate rise is unlikely to impact you. However, if your promotional period is due to end, or you are applying for a new credit card in the future, it is likely that your credit card provider will increase the Annual Percentage Rates (APR) for the card. A good way to avoid a rise in interest on your credit card is to complete a balance transfer, by transferring your existing credit card balance to a 0% balance transfer credit card. To ensure you pay no interest on your repayments, the balance needs to be repaid within the promotional interest-free period. Be aware that most (not all) balance transfer credit cards charge a balance transfer fee, usually between 2% and 5%. Find out more in our article, 'Best 0% balance transfer credit cards'.

Loans

If you already have a loan in place and it has a fixed interest rate then you are unlikely to be affected by the latest base rate rise. Those looking for a new loan are likely to see higher APR deals entering the market.

Overdrafts

The interest rate charged on your overdraft could be impacted by the latest rise in the Bank of England's base rate and so your rate could go up. You should receive advanced notification from your Bank or Building Society if this is the case, giving you time to consider your options.

How does the BoE interest rate rise affect you if you have savings?

Savings rates are likely to go up as a result of the latest Bank of England base rate rise, however, it is up to the individual bank or building society as to when they increase their rates. Some will take weeks or even months to increase rates following a Monetary Policy Committee announcement and others may not increase rates at all, as they are under no obligation to do so. If you are looking for the best savings rates then you should always shop around for the best deal. Check out the best savings rates using our Savings Best Buy tables.

If a link has an * beside it this means that it is an affiliated link. If you go via the link Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. But as you can clearly see this has in no way influenced this independent and balanced review of the product. The following link can be used if you do not wish to help Money to the Masses - Habito

MTTM AI (beta)

MTTM AI (beta)