Financial markets are pricing in a series of interest rate cuts throughout 2026 after official figures revealed a sharp rise in unemployment and a slowdown in wage growth. The latest data from the Office for National Statistics (ONS), released on Tuesday, shows that the UK unemployment rate has risen to 5.2% in the three months to December. This is the highest level since 2021.

Combined with cooling wage growth, analysts believe the Bank of England (BoE) now has enough evidence to cut interest rates as early as next month, with some forecasting that the base rate could fall from its current 3.75% to 3.00% by the end of the year.

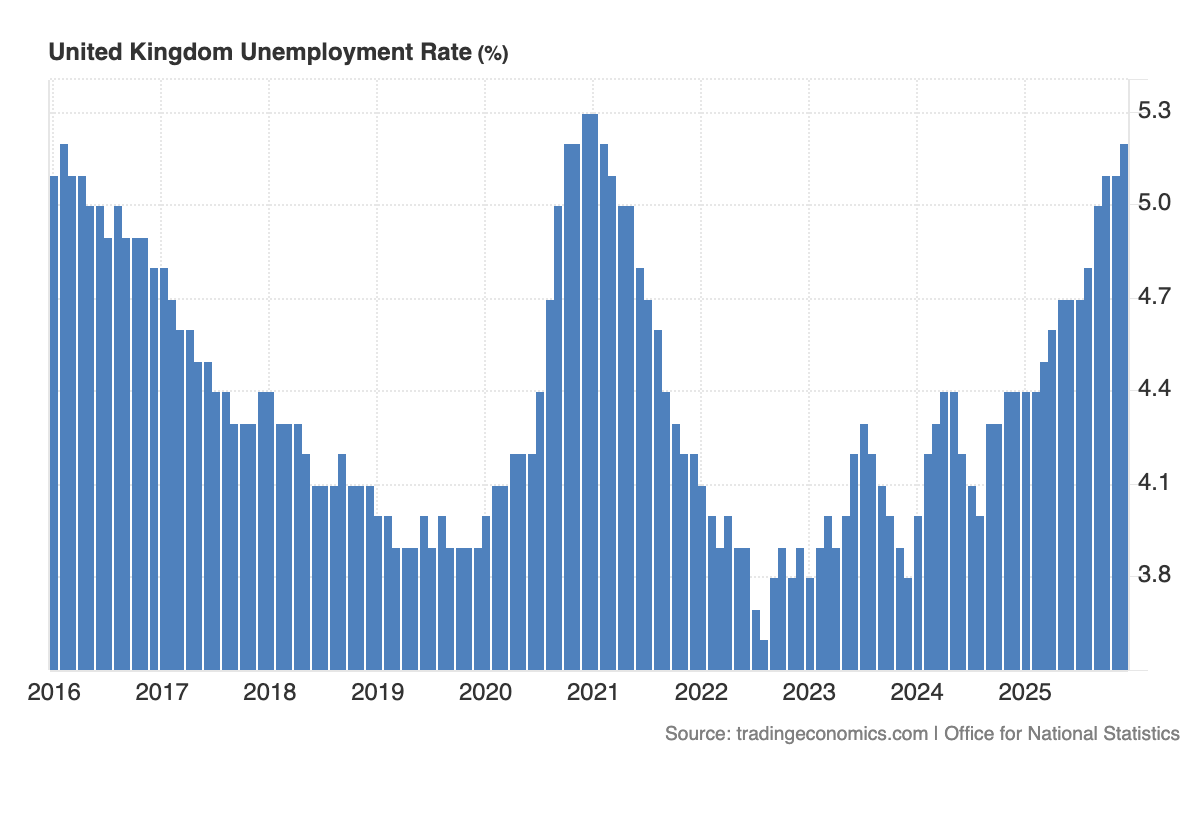

What does the latest UK jobs market data show?

The ONS figures paint a picture of a cooling jobs market, which is a key indicator the Bank of England watches when deciding on interest rates. The key takeaways from the report include:

- Rising unemployment: The UK unemployment rate rose to 5.2%, up from 5.1% in the previous quarter. This is the highest rate recorded since January 2021. To put this into context, the chart below shows the UK unemployment rate over the last 10 years. Notice how unemployment is almost back at the peak level of 5.3% experienced as a result of the Covid-19 pandemic.

- Slowing wage growth: Annual wage growth (excluding bonuses) has slowed to 4.2%. In the private sector, a metric closely watched by the BoE, pay growth fell to 3.4%, the lowest level in five years. Slowing wage growth reduces the pressure on companies to hike prices to cover their employee wage costs, which lowers the overall risk of inflation and gives the BoE the scope to cut interest rates. The latest UK inflation data is due to be released on 18th February and is expected to show that the annual rate of inflation has slowed to 3%.

- Youth unemployment: Younger workers appear to be the hardest hit, with the unemployment rate for 18-24 year-olds rising to 14%.

- Falling payrolls: The number of people on company payrolls fell by 11,000 in January, marking the fifth consecutive monthly decline.

How the jobs market data has impacted interest rate cut predictions

The BoE held the base rate at 3.75% at its meeting earlier this month. However, the continued weakening of the UK jobs market has strengthened the case for rate cuts to begin sooner rather than later. Market sentiment has shifted significantly, with current pricing implying a probability of around 80% that rates will be cut in March 2026. In total, the market believes there will now be two interest rate cuts of 0.25% in 2026, alongside the possibility of a third rate cut in the next 12 months.

Paul Dales, chief UK economist at Capital Economics, suggests the data support the view that the Bank has "at least a couple more interest rate cuts in its locker, with the chances of the next cut happening in March rather than April edging higher". Capital Economics forecasts that rates will fall to 3.00% this year, implying three cuts of 0.25% from the current level. Other analysts agree that the direction of travel is downwards. ING expects two rate cuts by June and that the unemployment rate could rise towards 5.5% in 2026. Deutsche Bank believes there will be just two more rate cuts this year by the summer.

Within the Bank of England’s own Monetary Policy Committee (MPC), there is already support for interest rate cuts. At the last meeting on 5th February, four of the nine MPC members voted to cut the base rate.

What does this mean for your finances?

If the market predictions are correct, which is not guaranteed, the landscape for borrowers and savers is set to change in the coming months.

Mortgage Borrowers

The prospect of falling interest rates is good news for mortgage borrowers. Swap rates, the rates at which lenders borrow money, often fall in anticipation of a base rate cut. This usually feeds through to cheaper fixed-rate mortgage deals.

If you are on a tracker mortgage, your monthly payments will fall immediately if the Bank of England cuts the base rate in the coming months. For those looking to remortgage, we may see lenders repricing their deals downwards in the coming weeks to stay competitive, although there is no sign yet that they are.

Savers

Conversely, a falling base rate is bad news for savers. As expectations of a rate cut solidify, banks and building societies tend to withdraw their best fixed-rate bond offers. If you have been waiting to lock away a lump sum, the window to secure the current top rates may be closing.

What should you do next?

- Monitor mortgage rates: If your mortgage deal is ending soon, keep a close eye on our best buy mortgage tables. With rates expected to fall, you may want to speak to a mortgage broker* about locking in a rate now that can be swapped for a cheaper one if prices drop further before your deal starts.

- Review savings interest rates: If you have cash in a variable rate savings account or are sitting on a lump sum, now is a good time to review the interest rate you are receiving on your savings and whether you can secure a better rate of interest, whether that be via an easy-access account or a fixed-rate bond. Make sure you check our regularly updated roundup of the best savings accounts in the UK.

If a link has an * beside it this means that it is an affiliated link. If you go via the link, Money to the Masses may receive a small fee, which helps keep Money to the Masses free to use. The following link can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers - Vouchedfor,

MTTM AI (beta)

MTTM AI (beta)