On 2nd November 2023, The Bank of England's (BoE) Monetary Policy Committee (MPC) voted for the Bank of England base rate to remain at 5.25%. The Bank of England base rate is at its highest level since March 2008 following consecutive rises between December 2021 and August 2023.

On 2nd November 2023, The Bank of England's (BoE) Monetary Policy Committee (MPC) voted for the Bank of England base rate to remain at 5.25%. The Bank of England base rate is at its highest level since March 2008 following consecutive rises between December 2021 and August 2023.

In this article, we explain the impact that the latest base rate decision will have on both savers and borrowers. We also include a number of additional resources and tools that may help those that are due to remortgage soon. For further information and predictions on where the Bank of England base rate is likely to be as we head into 2024, check out our interest rate forecast.

What is the Bank of England base rate?

The Bank of England base rate refers to the interest rate at which the Bank of England lends money to banks, building societies and other lenders. An increase in the Bank of England base rate usually signals an increase in the rate that banks and other lenders charge in order to maintain profitability. On the flip side, savers should be able to access improved savings rates, however, some providers can be slow to pass on the rise (if they do at all) and so it is worth comparing the best savings rates on offer.

Why has the Bank of England base rate remained the same?

Nine people sit on the Bank of England's Monetary Policy Committee (MPC) which meets every 6 weeks to decide on the Bank of England base rate. On 2nd November, 6 members voted to keep the Bank of England base rate at 5.25% while 3 others voted to increase the rate by a further 0.25% to 5.50%. The rate was predicted to remain at 5.25% and so this has not come as a huge surprise.

The Bank of England uses the base rate to help control inflation. The current rate of inflation in the UK as measured by CPI is 6.7% which remains much higher than the 2% target. Despite this, the rate of inflation is expected to fall as we head into 2024 with experts predicting that it will reduce to 3.75% by Q2 of 2024.

A statement on the Bank of England website said that the 'MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee’s remit. The MPC’s latest projections indicate that monetary policy is likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures'.

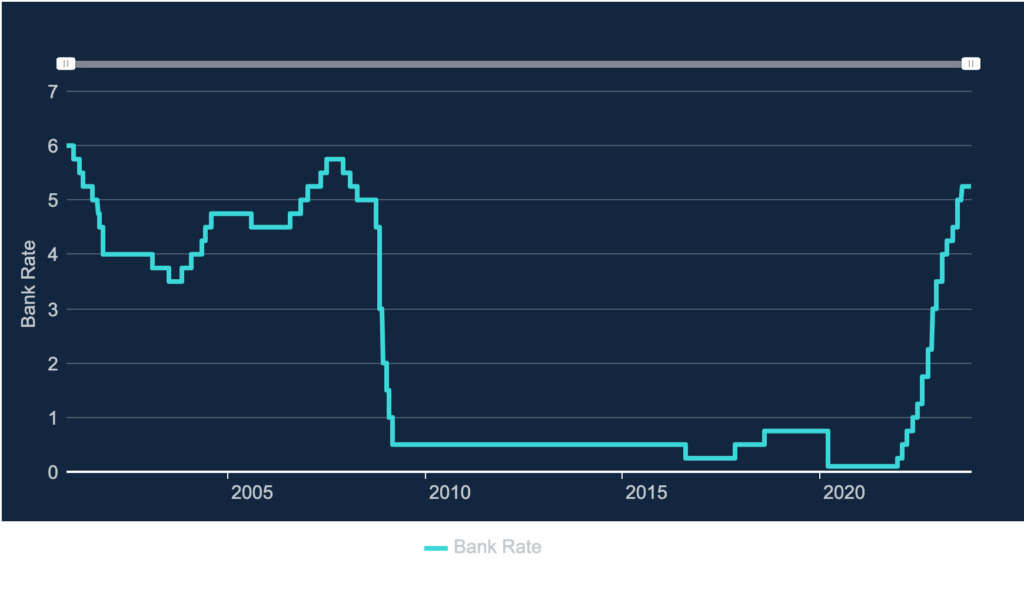

How has the bank rate increased over time?

The following graph shows how the Bank of England base rate has increased over time.

(Source: Bank of England)

Rate rises and how they impact you: December 2021 - August 2023

The Bank of England last raised the base rate in August 2023 with the increase aimed at reducing inflation. Below, we provide a summary of the Bank of England base rate rises since December 2021, which was when the BoE began its series of aggressive increases.

| Date | Interest rate rise | Previous interest rate | New interest rate | Increase to average monthly mortgage repayments per £100k borrowed* |

| 16th December 2021 | +0.15% | 0.10% | 0.25% | £8 |

| 2nd February 2022 | +0.25% | 0.25% | 0.50% | £13 |

| 17th March 2022 | +0.25% | 0.50% | 0.75% | £13 |

| 5th May 2022 | +0.25% | 0.75% | 1.00% | £13 |

| 16th June 2022 | +0.25% | 1.00% | 1.25% | £13 |

| 4th August 2022 | +0.50% | 1.25% | 1.75% | £26 |

| 22nd September 2022 | +0.50% | 1.75% | 2.25% | £26 |

| 2nd November 2022 | +0.75% | 2.25% | 3.00% | £39 |

| 15th December 2022 | +0.50% | 3.00% | 3.50% | £26 |

| 2nd February 2023 | +0.50% | 3.50% | 4.00% | £26 |

| 23rd March 2023 | +0.25% | 4.00% | 4.25% | £13 |

| 11th May 2023 | +0.25% | 4.25% | 4.50% | £13 |

| 22nd June 2023 | +0.50% | 4.50% | 5.00% | £26 |

| 3rd August 2023 | +0.25% | 5.00% | 5.25% | £13 |

| TOTAL | £268 |

*assumed mortgage term is 25 years

How does the BoE interest rate review affect you if you have a mortgage?

Fixed-rate mortgage customers

Those on a fixed-rate mortgage will not see a change to the interest rate they pay until their mortgage deal term comes to an end. However, if your deal is due to come to an end soon, you should consider how the previous bank rate rises will affect the new rate that you are able to secure. Our article 'Remortgaging in 2023 – is now the right time to fix & for how long?' provides further insight into remortgaging and what to do if you are due to remortgage in the coming months.

To provide some basic calculations, the last 0.25% rise in August will mean that your monthly mortgage repayments, based on a 25-year mortgage term, could increase by approximately £13 per month for every £100,000 borrowed. It is worth remembering, however, that these figures only take into consideration the latest base rate rise, so if your existing fixed-rate deal was in place prior to December 2021 (when rates first started to rise), then you should factor in all of the interest rate rises combined. This equates to a rise of around £268 per month, per £100,000 borrowed, based on a 25-year mortgage term as shown in the table above.

Variable rate or tracker mortgage customers

As the Bank of England base rate has remained the same, those with tracker or variable rate mortgages may not see their mortgage payments change. You can, however, use our interest rate rise calculator to work out what the impact will be on your mortgage payments. You'll need to know your initial mortgage term, the amount borrowed at the start of the deal and your current mortgage rate.

Anyone worried about the impact the base rate will have on their finances should speak with an independent mortgage adviser* as they can easily explain the likely impact on your finances and also provide advice on remortgaging. They will be able to weigh up your options and compare what mortgage rates and deals are available to you. Always check to see if there are any Early Repayment Charges (ERC) when remortgaging and check to see how long is left on your current mortgage deal. Also, you can take a look at the best mortgage deals yourself by using our mortgage rate comparison tool.

Help if you're unable to afford your mortgage payments

If you're having trouble paying your mortgage or are worried about how you will afford your mortgage due to higher interest rates as well as increases to the cost of living then you should get in touch with your lender as soon as possible. Your lender may be able to provide support and it is in their interest to find a solution to ensure that mortgage repayments are not missed. Potential solutions could include allowing you to take a mortgage payment holiday, extending the length of your mortgage or converting part or all of a repayment mortgage to interest-only in order to reduce your monthly repayments.

You may also find additional support from the following organisations helpful:

How does the BoE interest rate review affect you if you have credit cards, loans or overdrafts?

Credit cards

It is unlikely that your credit card provider will increase the Annual Percentage Rates (APR) on your credit card and if you have an existing credit card with an agreed interest-free period or promotional interest rate you won't notice any immediate impact from any Bank of England rate changes. However, if your promotional period is due to end, or you are applying for a new credit card in the future, you will likely notice that the APR is higher than it was before.

One way to avoid a rise in interest on your credit card is to complete a balance transfer, by moving your existing credit card balance to a 0% balance transfer credit card. To ensure you pay no interest on your repayments, the balance needs to be repaid within the promotional interest-free period. Be aware that most (not all) balance transfer credit cards charge a balance transfer fee, usually between 2% and 5%, and of course, you will be credit-checked during the application process. Find out more in our article, 'Best 0% balance transfer credit cards'.

Loans

If you already have a loan with a fixed interest rate then you are unlikely to be affected by changes to the base rate. If you are looking for a new loan then you can compare the best loan deals in our article, 'Best personal loans'.

Overdrafts

As the Bank of England's base rate has not changed, the interest rate charged on your overdraft is likely to remain the same. However, if your Bank or Building Society is going to change the rate of interest charged, you should receive a notification in advance, giving you time to consider your options.

How does the BoE interest rate review affect you if you have savings?

As the Bank of England base rate has remained the same since September it is possible that we may have hit the peak of high interest rates on savings accounts. Therefore, if you are looking to maximise your savings, now might be a good time to secure one of the best rates. Our article, 'How to get over 5% on your savings' summarises some of the best rates on the market and our regularly updated article, 'Best savings accounts in the UK' is continuously updated with the best savings rates for personal and business accounts.

If you are looking for the best savings rates then you should always shop around for the best deal. You can also check out the best savings rates using our Savings Best Buy tables. Right now you can get as much as 8.00% interest on a Regular Saver account.

If a link has an * beside it this means that it is an affiliated link. If you go via the link Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. But as you can clearly see this has in no way influenced this independent and balanced review of the product. The following link can be used if you do not wish to help Money to the Masses - VouchedFor

MTTM AI (beta)

MTTM AI (beta)