Hargreaves Lansdown* launched its ready-made pension plan in November 2023 with the aim of providing a simple, low-cost investment solution for those investing in a SIPP (Self-invested personal pension). In December 2022, the Financial Conduct Authority (FCA) set out new rules to improve outcomes for consumers investing in non-workplace pensions, which included platforms needing to offer a standardised 'default' investment option. The Hargreaves Lansdown ready-made pension has two investment stages with the first stage aimed at growing your money when you’re younger, before moving to stage two, investing in lower-risk assets as you approach retirement.

Hargreaves Lansdown* launched its ready-made pension plan in November 2023 with the aim of providing a simple, low-cost investment solution for those investing in a SIPP (Self-invested personal pension). In December 2022, the Financial Conduct Authority (FCA) set out new rules to improve outcomes for consumers investing in non-workplace pensions, which included platforms needing to offer a standardised 'default' investment option. The Hargreaves Lansdown ready-made pension has two investment stages with the first stage aimed at growing your money when you’re younger, before moving to stage two, investing in lower-risk assets as you approach retirement.

In this article, we explain how the Hargreaves Lansdown ready-made pension works, how much it costs and finally how it compares to other ready-made pension plans from its competitors.

What is the Hargreaves Lansdown ready-made pension?

Hargreaves Lansdown's ready-made pension plan is the default investment option for those looking to invest in a SIPP and who are happy to let someone else manage their investments for them. Its team of investment experts will actively manage the portfolio of investments on the investor's behalf, handling all of the day-to-day investment decisions. A ready-made pension may be a good option for those who are new to investing or who do not have the time to manage the investment decisions themselves.

How does the Hargreaves Lansdown ready-made pension work?

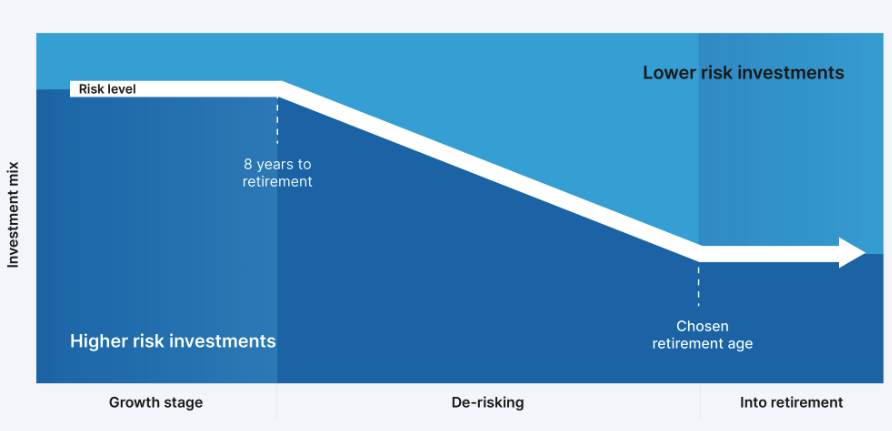

The Hargreaves Lansdown ready-made pension plan has two stages. The growth stage and the de-risking stage. Below we explain how each of the stages work.

Hargreaves Lansdown ready-made pension - Growth Stage

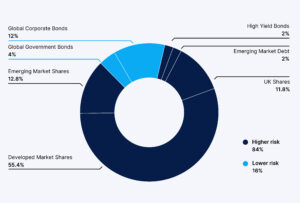

Investors who are more than 8 years from retirement will initially be invested in the HL Multi-Index Moderately Adventurous fund, a fund designed to help investors grow their money while they are younger. This is referred to as the 'growth stage'.

HL Multi-Index Moderately Adventurous fund - Asset mix

Hargreaves Lansdown ready-made pension - De-risking Stage

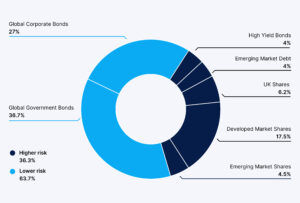

Then, when the investor is 8 years from their chosen retirement age, investments in the HL Multi-Index Moderately Adventurous fund will gradually be sold in favour of the lower-risk HL Multi-Index Cautious fund. Hargreaves Lansdown calls this the 'de-risking' stage, however, in investing terminology, it is often referred to as 'lifestyling' - a process designed to reduce the impact of stock market volatility as you get closer to retirement. Anyone joining the plan who has less than 8 years before their chosen retirement age, will have their investments split proportionally between the two funds.

HL Multi-Index Cautious fund - Asset mix

How much does the Hargreaves Lansdown ready-made pension cost?

The cost of the Hargreaves Lansdown ready-made pension will depend on the amount you wish to invest. Hargreaves Lansdown's account fee is tiered, meaning you could end up paying less as you invest more. For more information on Hargreaves Lansdown's fees, check out our full independent Hargreaves Lansdown review.

Below, we've provided the fees you will pay on the Hargreaves Lansdown ready-made pension, based on a pot totalling less than £250,000.

| Fee type | % fee |

| Hargreaves Lansdown account charge | 0.45% |

| Hargreaves Lansdown plan management fee | 0.30% |

| Total Fee | 0.75% |

Additional fund fees apply such as transaction charges, meaning the total average charge is around 0.85%.

What is the minimum investment amount?

You can invest in the Hargreaves Lansdown ready-made pension* with either a minimum £100 lump sum investment via a debit card, or alternatively, you can start by setting up a regular personal contribution of £25 per month.

Should I invest in the Hargreaves Lansdown ready-made pension?

Hargreaves Lansdown's ready-made pension provides investors with a simple, low-cost way to invest in a SIPP. It may be a good option for those who are new to investing or simply do not have the time or inclination to handle the investment decisions themselves. The plan is simple in that it invests in a single 'moderately-adventurous' fund before transitioning to a 'cautious' fund as the investor gets closer to retirement. Whether you should invest in the ready-made pension plan is ultimately down to you, however, it is worth considering the alternatives as there may be a more suitable solution for you.

Hargreaves Lansdown ready-made pension alternatives

Below we look at some alternatives to the Hargreaves Lansdown ready-made pension. You may also want to take a look at our article 'Best ready-made pension in the UK'.

Robo-advice platforms

There are a number of robo-advice platforms that offer fully managed, ready-made pension plans and these include Wealthify, J.P. Morgan Personal Investing and Moneyfarm*. Some will even let you invest from as little as £1 and, depending on the amount you invest, fees can be as low as 0.35%. This is lower than the Hargreaves Lansdown ready-made pension.

Nest

There are alternative ready-made pension plans that take the multi-stage approach further, such as the Nest Retirement Date fund. Its four-phase approach, similar to Hargreaves Lansdown, includes a growth and de-risking phase, however, it also includes a 'foundation phase' aimed at higher growth for younger investors and a 'post-retirement' phase aimed at maximising returns whilst in retirement. It also comes in cheaper than Hargreaves Lansdown with an annual management charge of just 0.30%, however, it does charge a 1.8% fee on all contributions.

Other investment platforms

If you like the idea of investing in a ready-made pension via an investment platform then there are some alternatives you could consider. Interactive Investor* offers six 'quick-start' funds and its 'Pension Essentials' plan charges a flat fee of just £5.99 per month. Alternatively, Bestinvest* offers a number of ready-made portfolios to choose from with annual fees starting at just 0.20%. It also pays 3.23% interest on uninvested cash.

Pros and cons of the Hargreaves Lansdown ready-made pension

Pros

- Experts take care of the investment decisions

- Simple set-up process

- The plan lowers in risk as you get closer to retirement

Cons

- Fees are higher than some alternative DIY options

- You cannot make changes to the funds you are invested in

- The investment option is limited compared to ready-made options available elsewhere

Summary

Hargreaves Lansdown's ready-made pension* could be a good solution for someone looking to invest in a simple, diversified pension portfolio. Its two-stage approach is designed to lower investment risk as the investor approaches retirement and so is likely to appeal to those who wish to have a fairly hands-off approach to investing. That being said, there are cheaper ready-made options available (mentioned earlier) as well as other ready-made solutions that go further than the two-stage solution offered by Hargreaves Lansdown.

When investing, your capital is at risk and you may get back less than invested. Past performance doesn’t guarantee future results.

If a link has an * beside it this means that it is an affiliated link. If you go via the link, Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. The following links can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers - Hargreaves Lansdown, Interactive Investor, Moneyfarm, Bestinvest

MTTM AI (beta)

MTTM AI (beta)