The average rate of interest on a two-year mortgage deal has dropped below 5% for the first time in almost three years, according to new data from Moneyfacts. The figure has held stubbornly above 5% ever since the disastrous 2022 mini-budget of then-Prime Minister Liz Truss, so this shift provides some welcome relief for borrowers. However, it may not herald the plummeting rates that many are hoping for.

The average rate of interest on a two-year mortgage deal has dropped below 5% for the first time in almost three years, according to new data from Moneyfacts. The figure has held stubbornly above 5% ever since the disastrous 2022 mini-budget of then-Prime Minister Liz Truss, so this shift provides some welcome relief for borrowers. However, it may not herald the plummeting rates that many are hoping for.

Announcing the new figure, Adam French, head of news at Moneyfacts, said: “While the cost of borrowing is still well above the rock-bottom rates of the years immediately preceding that fiscal event, this milestone shows lenders are competing more aggressively for business.

“However, while mortgage rates have followed the mood music set by successive cuts to the Bank of England base rate, homeowners and first-time buyers may have to wait longer for more substantial cuts.”

Why have mortgage rates dropped?

The Bank of England has cut the base rate five times in the last 12 months, and this has been reflected in a steady drop in mortgage rates. The most recent cut of 0.25% announced last week has been enough to finally get the two-year fix average mortgage rate below 5%, but anyone looking to buy a new home or remortgage soon should not get too excited. Inflation is currently well above the Bank’s target of 2%, with forecasts of a further spike this Autumn, while the decision to cut rates last week was passed by the narrowest of margins. This means that further reductions to mortgage costs this year are not guaranteed.

Adam French, head of news at Moneyfacts, said that while the average mortgage rate may have reached “a symbolic turning point”, inflation is not expected to hit the BoE’s target “until 2027 or beyond, which is likely to mean the base rate will hold around its current level for longer.”

The drop in average mortgage rates could also be attributed to growing competition among mortgage providers, with lenders operating at increasingly tight margins in order to attract customers.

Is 5% a good mortgage rate?

Ultimately, a good mortgage rate will be the best one available to you when you come to buy or remortgage.

While the average two-year fixed rate mortgage deal may have slipped below 5% this month, the best rates have been well below 5% for some time. Currently, borrowers with a 40% deposit can get a mortgage rate of 3.73% from RBS, those with a 20% deposit can get 3.9% from YBS and those with a 10% deposit can get 4.18% from HSBC. Whether or not you can get one of these top deals will depend on your personal financial circumstances, but it is important to remember that the average figure is not necessarily what you will pay. Go to our 'Best mortgage rates in the UK' page to see the latest top deals.

How have mortgage rates changed in recent years?

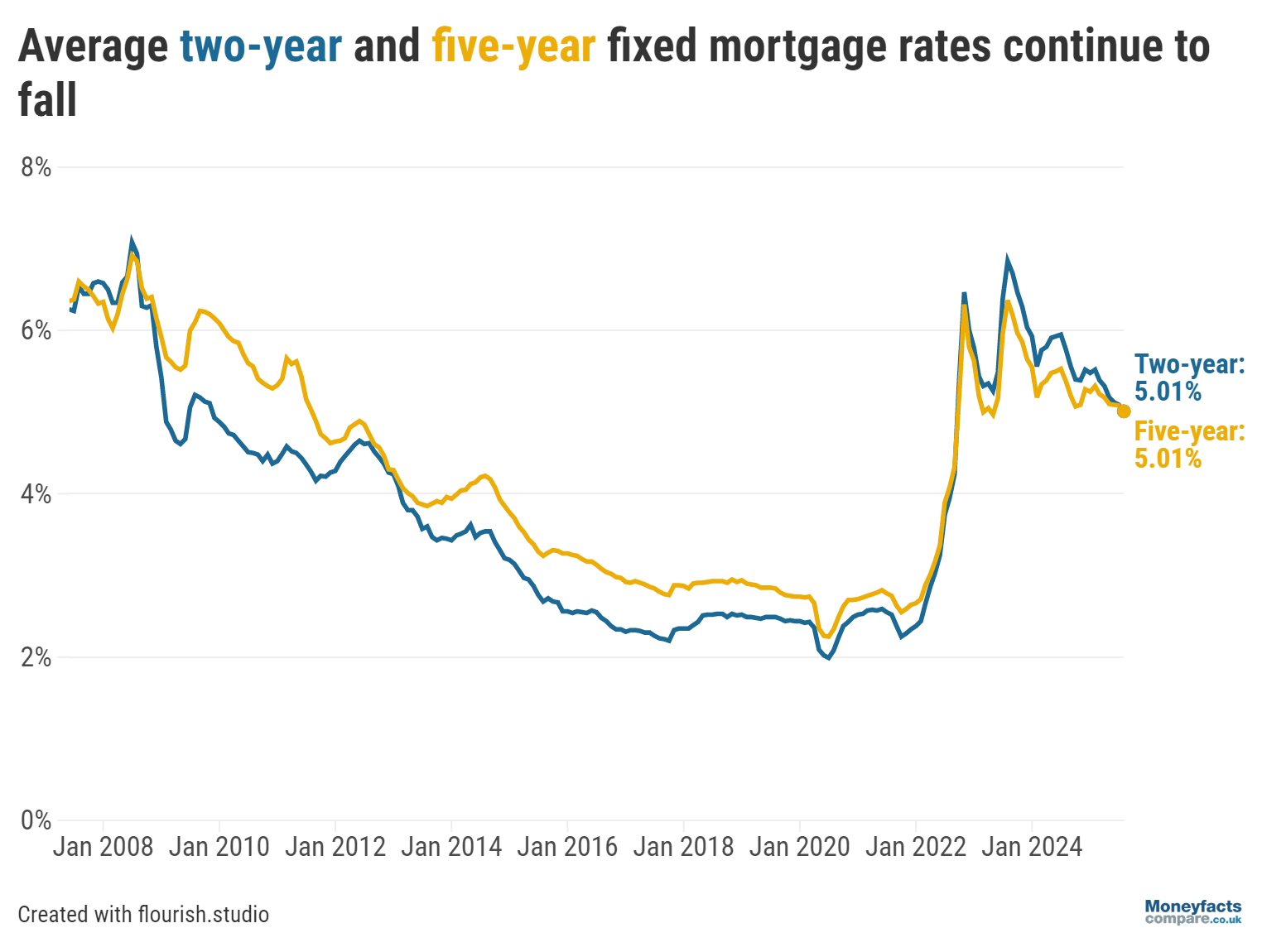

You can see from the graph below, which was produced by Moneyfacts, how the average interest on a two-year and five-year fixed mortgage deal has fluctuated in recent years. Both have hovered around 5% for some time before the two-year average finally dipped this week. However, that eventual breakthrough is put into context by the dramatic climb of 2021-2022, which is still impacting borrowers across the UK. Banking industry group UK Finance estimates that 1.6m fixed rate mortgages have expired in 2025 or are due to expire this year, meaning a huge number of households who may not have remortgaged since 2020 will be desperately hoping for this graph to take another dip before their current deal ends.

How to get the best mortgage rate

As mortgage rates regularly change, the easiest way to check for the best current deals is by using our mortgage rate comparison tool. The tool will find some of the best mortgage interest rates available for the amount of money you need to borrow based on your loan-to-value ratio. Keep in mind that other factors, including your income, outgoings, credit score and borrowing history will affect whether or not you qualify for those mortgage deals. We provide specific guidance around finding the best mortgage deals in our articles, 'How to get the best mortgage deal' and 'How to remortgage and get the best rate'.

To get the best mortgage rate for your specific needs, you could speak with a mortgage broker – ideally one who has access to the whole mortgage market. Mortgage brokers not only have expertise in understanding how to get the best mortgage rate for your circumstances, but they can also access deals that may not be offered to consumers directly.

You can source a vetted mortgage professional locally using VouchedFor* – make sure to read our article 'How to find a mortgage broker you can trust' first – or you can get in touch with the online mortgage broker, Habito*, which has an efficient mortgage search tool, an online chat service and access to over 90 lenders.

If a link has an * beside it this means that it is an affiliated link. If you go via the link, Money to the Masses may receive a small fee, which helps keep Money to the Masses free to use. The following link can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers - Habito, Vouchedfor

MTTM AI (beta)

MTTM AI (beta)