Savers looking to make the most of their tax-free allowance are seeing a major shift in the savings market. One-year fixed-rate Cash ISAs are once again offering higher returns than easy-access Cash ISAs, with the very best fixed deals offering interest of up to 4.70% AER. This marks a change from recent months, where easy-access accounts dominated the top of the cash ISA best-buy tables.

Savers looking to make the most of their tax-free allowance are seeing a major shift in the savings market. One-year fixed-rate Cash ISAs are once again offering higher returns than easy-access Cash ISAs, with the very best fixed deals offering interest of up to 4.70% AER. This marks a change from recent months, where easy-access accounts dominated the top of the cash ISA best-buy tables.

Why Fixed-rate Cash ISAs are now beating easy-access

In the run-up to the end of the tax year on 5th April, providers frequently used temporary bonus rates to attract customers to their easy-access ISA products. With the new tax year now underway, the market has settled and many of these introductory bonuses have been withdrawn or reduced. As a result, we have started to see the underlying interest rates on easy-access ISAs fall.

At the same time, interest rates on one-year fixed-rate ISAs have started to increase due to recent global events and rising inflation. While the Bank of England's base rate is currently held at 3.75%, the conflict in the Middle East has pushed energy and oil prices higher. This has caused UK inflation to tick back up to 3.3% and it is expected to rise further in the coming months.

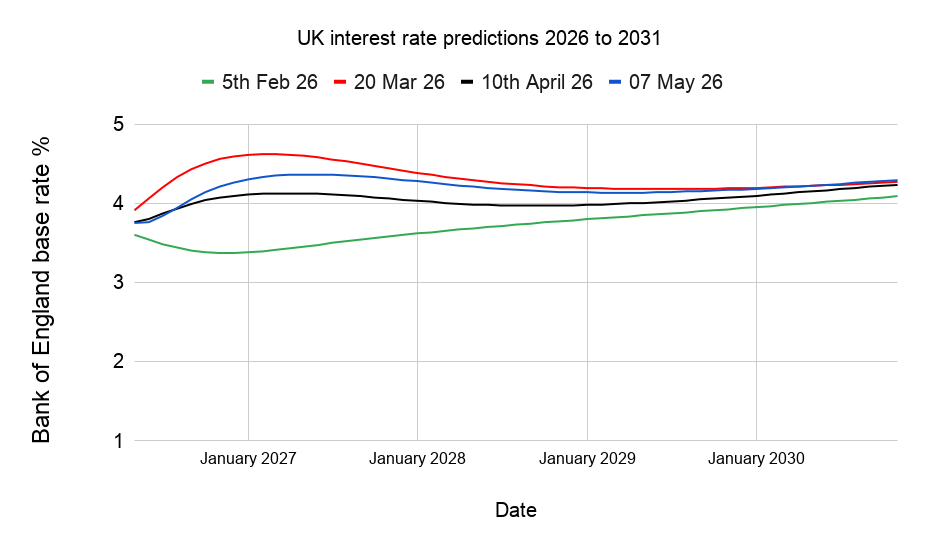

To help fight rising inflation, financial markets predict that the Bank of England will be forced to increase the base rate over the coming year, potentially reaching 4.25% by 2027 (see chart below). When market expectations rise, it becomes much more expensive for banks to borrow money from other financial institutions. Instead, it is usually more cost-effective for them to turn to everyday savers. Because a fixed-rate ISA locks your money in for a set period, it provides banks with the stable funding they need to offer long-term loans and mortgages. Providers are willing to offer a premium interest rate today because locked-in savings are a reliable, cheaper alternative to borrowing elsewhere.

Latest Bank of England base rate predictions

Best Cash ISA rates

Below, we compare the best easy-access and fixed-rate Cash ISAs available on the market. The interest rates shown are correct at the time of publication.

Best easy-access Cash ISA rates

Updated: 11/05/2026

Best fixed-rate Cash ISA rates

| Meteor Savings provided by AlRayan Bank | Meteor Savings provided by AlRayan Bank | Nationwide | United Trust Bank | Hargreaves Lansdown | |

| Account name | 1 Year Fixed Rate Cash ISA | 2 Year Fixed Rate Cash ISA | 3-Year Fixed Rate Cash ISA | 4 Year Fixed Rate Cash ISA | 5-Year Fixed Rate Cash ISA* |

| AER | 4.70% | 4.65% | 4.60% | 4.00% | 4.55% |

| Minimum opening balance | £1,000 | £1,000 | £1 | £20,000 | £1,000 |

| How to manage the account | Online | Online | Online, Branch, Mobile Banking | Online, Post Telephone | Online |

| How to apply | Online | Online | Online, Branch, Mobile | Online | Online |

| Accepts cash ISA transfers in? | Yes | Yes | Yes | Yes | Yes |

| Accepts stocks & shares ISA transfers in? | Yes | No | Yes | No | Yes |

| Financial Services Compensation Scheme | Own Licence | Own Licence | Shared Licence | Own Licence | Own Licence |

Source: theprivateoffice.com: Updated 11/05/2026

Pros and Cons for Savers

Deciding between a fixed-rate and an easy-access Cash ISA depends entirely on your personal circumstances and when you might need to access your money.

Pros and Cons of fixed-rate Cash ISAs

- Pros - The interest rate is guaranteed for the duration of the term, providing certainty over your returns. This also protects savings from any potential interest rate cuts during the fixed period.

- Cons - Funds are typically locked away for the entire term. Accessing the money early usually incurs a penalty, such as the loss of 90 days' interest. Furthermore, if interest rates unexpectedly rise, the account will not benefit from the higher market rates.

Pros and Cons of easy-access Cash ISAs

- Pros - These accounts offer high flexibility, allowing savers to withdraw funds whenever needed without facing financial penalties. This makes them an ideal home for an emergency fund. Savers are also free to move their money to a different provider if a better rate becomes available.

- Cons - The interest rate is variable, meaning the provider can reduce it at any time. Additionally, the highest rates often rely on temporary bonuses that expire after a set period, requiring savers to monitor their accounts and switch regularly to secure the best return on their money.

MTTM AI (beta)

MTTM AI (beta)