Episode 418 - On this week's episode, I explain the concept of value averaging as an alternative investment strategy to achieve a specific future monetary goal. Then, I address frequently asked questions related to pensions which have emerged from recent live events I’ve participated in. Finally, Andy provides a quick update on house prices, explaining the significance of recently released data.

Join the MTTM Community group, a friendly community that allows like-minded listeners to ask questions and chat.

You can also listen to other episodes and subscribe to the show by searching 'Money to the Masses' on Spotify or by using the following links:

Abridged transcript of Episode 418

Netwealth’s wealth management service combines a comprehensive low-cost investment solution with access to qualified advisers.

They recently launched MyNetwealth – a digital dashboard that combines all your savings and investments – from multiple providers – in one place.

MyNetwealth's wealth planner tool helps you visualise your current wealth and apply it to your future needs. It takes into account various factors such as age, investments, pensions, tax wrappers, and expected contributions or withdrawals – and calculates the likelihood of you achieving your goals. Daily updates make it easy to track the value and performance of your wealth.

MyNetwealth also provides a library of useful personal finance content and if you ever need advice or guidance, their highly qualified team is always there to help.

You can find out more information and sign up for MyNetwealth in 30 seconds visit my.netwealth.com. Please remember, the value of investments can go down as well as up, so you may get back less than you invest.

Value averaging

On this part of the podcast I discuss value averaging as an investment strategy and compare it to pound cost averaging and lump sum investing, including its pros and cons. Some of the insights include:

- Value averaging is a strategy where you adjust your regular investment amount based on a target value you want to achieve in the future.

- The goal of value averaging is to reach a predetermined target value over time, regardless of market conditions.

- Unlike pound cost averaging, where you invest equal amounts over time, value averaging involves adjusting your contributions based on the portfolio's performance at each point that you make a contribution.

- If the portfolio falls behind the predicted value when you are due to make a contribution, you increase your contributions to catch up, buying more shares or units in a fund when the market is low.

- If the portfolio exceeds the expected value, you can reduce your contributions or sell some investments to bring it back in line with the expected value at that point.

- Value averaging enforces disciplined investing behaviour by buying low and selling high, aiming to optimise long-term returns.

- It also provides a systematic approach that removes emotional decision-making from the investment process.

- The big disadvantage is that value averaging can be time-consuming and requires initial setup calculation with realistic assumptions and a cash pool to invest additional funds if needed in the future.

- Value averaging can outperform pound cost averaging during periods of significant market fluctuations and declines.

- Luck and timing ultimately play a role in value averaging, just like in other investment strategies.

- Value averaging may appeal to those wanting to achieve a set target amount by a specified future date and who are willing to take risks and invest more during market downturns.

Pension FAQs

In this section of the podcast I discuss the most popular questions I am asked about pensions and retirement planning at live events. Some of my key insights are given below:

- The amount of money needed for a decent standard of living in retirement varies based on lifestyle choices. The PLSA (Pensions and Lifetime Savings Association) Retirement Living Standards provide figures based on the annual income needed for a comfortable retirement, categorised into three levels: minimum, moderate, and comfortable. You can find the latest figures in the resources section below.

- The 4% rule for a sustainable withdrawal rate from a defined contribution pension is a broad guideline, but a more realistic range is between 1.8% and 3% as we explained in episode 210 of the MTTM podcast (see resources section below)

- Annuities are becoming popular again due to increased annuity rates resulting from higher gilt yields. Currently a 65 year old can get over 7% for an annuity with a 5 year guarantee period. This is twice the level achievable at the start of 2022.

- Consider using retirement calculators (see link to our pension calculator in the resources section below) to estimate the income you can expect from your pension and plan accordingly.

- Visualise your ideal retirement by thinking about what you don't want it to be and working towards what you do want.

- Have conversations about money with your partner.

- Make sure you take advantage of auto-enrolment via a company pension scheme and employer pension contributions if you are employed.

- The general rule of thumb for pension contributions is to contribute at least half your age as a percentage of your income if you've not started already.

- Starting early with pension contributions can take advantage of the power of compounding, while delaying contributions will require significantly larger monthly amounts to achieve the same retirement income. A 25 year old investing £200 a month (£100 employee and £100 employer contributions) over 40 years will retire at 65 with a pension pot worth over £500,000. A 45 year old starting to contribute to their pension would have to invest a total of around £1,000 a month to achieve the same result.

- Unconventional retirement approaches, such as generating income from hobbies or passions, can help supplement retirement funds.

- Carry forward rules allow for unused pension allowances from previous tax years to be used, but you must have been a member of a pension for the entire period to take advantage of the rules.

- Retirement spending habits can change over time, with spending increasing slightly in the early years and then shifting towards different categories of expenses later on - listen to MTTM podcast 372 below for more information.

- Freelancers should still put money aside for retirement, even though they don't benefit from auto-enrolment.

- Directors of businesses should remember to prioritise their own pension contributions, with gross pension contributions paid by the company usually being the most tax-efficient way to do this.

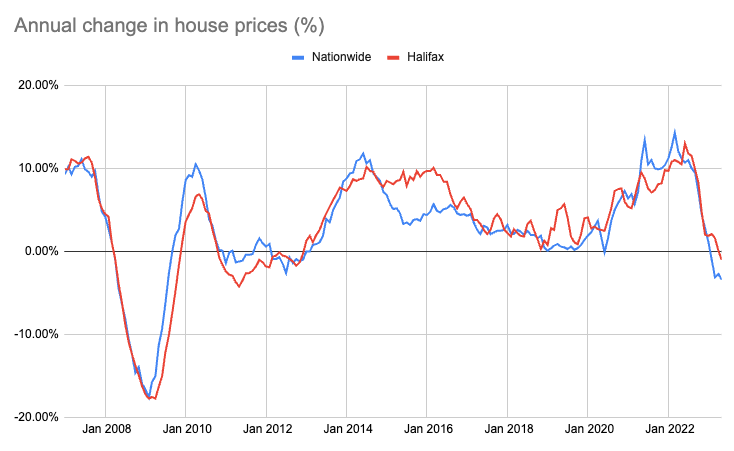

House price highlights

In this section of the podcast we discuss the latest house price data and explain the chart below.

Sponsor

Thank you to our podcast sponsor:

Netwealth - For more information about Netwealth, please check out our Netwealth review.

Please remember, with investing your capital is at risk and the value of investments can go down as well as up, so you may get back less than you invest. Netwealth is authorised and regulated by the Financial Conduct Authority.

Resources

Links referred to in the podcast:

- Value averaging spreadsheet

- MTTM - Ep 332 - Pound cost averaging weakness

- MTTM Podcast 210 – Debunking the 4% rule

- Pension Calculator

- Pension carry forward rules explained

- MTTM Podcast Episode 372 – Retirement spending truths

- PLSA Retirement Living Standards

- VouchedFor review

- Halifax records first annual fall in house prices in 11 years

- What is going to happen to house prices?

Data sources: Halifax, Nationwide

MTTM AI (beta)

MTTM AI (beta)